Contact us on [email protected] to request a quote

| Blogs

The cost of many raw materials, including high-performance metals such as stainless steels and nickel alloys, remains volatile. Each month seems to bring a fresh challenge, so we thought it worthwhile sharing some insight into the main drivers behind price changes.

It would be difficult to avoid starting with nickel costs, even though its price has been relatively stable in recent weeks. However, as the most expensive alloying addition to our range of alloys, any change feeds through to the metal price very quickly.

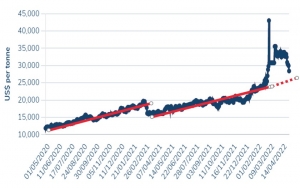

In early March, the London Metal Exchange (LME) index had been increasing steadily towards $25,000/T. It had generally been rising for more than 2 years, but the rate of change was increasing, perhaps as the world emerged from the effects of Covid and the supply-demand balance shifted. However, the price spiked to $44,000/T and then $101,000/T in the space of a day before trading was suspended. This was associated with the action of various traders, rather than the underlying demand for this important metal. However, it took more than three weeks for ‘orderly trading’ to be restored, and for steel mills to feel sufficiently confident to re-issue price lists – albeit with nickel now trading at >$33,000/T.

The LME index has drifted down towards $28,000/T since then, meaning that the nickel element of the steel mills ‘alloy surcharges’ will reduce over the next couple of months – as there is typically a lag between the LME index and alloy surcharges, reflecting the time it takes to purchase and consume raw materials in the steelmaking process.

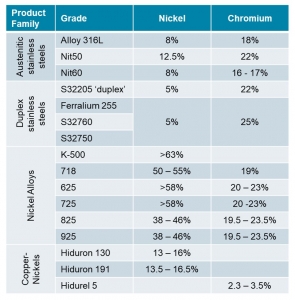

It should be noted that the impact of nickel price volatility on duplex and super duplex stainless steels is far less than most other alloys. They contain just 5% nickel, compared with 8% for Alloy 316L, >12% for Nit50, and 45-65% for nickel-based alloys such as Alloy 625, 718, 725, 825, 925 or K-500.

Chromium is the primary alloying addition to turn a steel into stainless steel – a minimum of 10.5% required to form the protective ‘passive layer’. It is added as ‘ferrochrome’, the price of which has increased dramatically from February 2022 onwards.

Ferrochrome is predominantly mined in South Africa, although there are significant deposits in Turkey, Kazakhstan, India and Finland. It is not openly traded on the LME, so pricing information is less visible.

Heavy rains and flooding in South Africa have certainly disrupted mining activity, but increasing energy costs are the main driver behind these price rises – ferrochrome is produced by refining chromite ore in an electric arc furnace, which consumes significant quantities of expensive electricity.

The price of ferrochrome has increased by more than 50% since February. As a ‘regular’ 316 stainless steel would contain 18% chromium, a duplex would contain 22%, super duplex 25% and between 18-23% for most of the nickel-based alloys we stock, ferrochrome increases will be impacting the May-onwards alloy surcharge.

Mill production orders are still subject to energy and transport surcharges. Although much smaller than the alloy surcharge – adding up to 5% of the total delivered price – they continue to nudge upwards.

Mill lead times are generally 7months+ for most stainless steel and nickel alloys. Smaller diameter bars, or those alloys requiring re-melting or additional heat treatment may take longer to produce. The longest lead time product in our stock programme is currently 18 months! However, this is an exception, and we have considerable incoming deliveries throughout May and June 2022 as part of our routine re-ordering pattern.

There are a number of ways we can help you manage your sourcing requirements to reduce uncertainty, please contact us today.

Global Delivery Available

Air, sea, and road freight options are available, with a range of packaging solutions, to support global deliveries.

Inventory Management

Let us manage your total material requirements with call-off and consignment arrangements.

Up to 40 sizes per alloy available

More sizes equal less machining and a more cost-effective supply chain.